")

4kodiak/iStock Unpublished via Getty Images

Amazon released its third quarter results

Amazon (NASDAQ:AMZN) will report its third quarter financial results on Thursday, October 27, 2022, after market close. Anyone interested can follow the call live on Amazon’s Investor Relations website here. Seeking Alpha will also release a handy transcript of the call this page after it’s done.

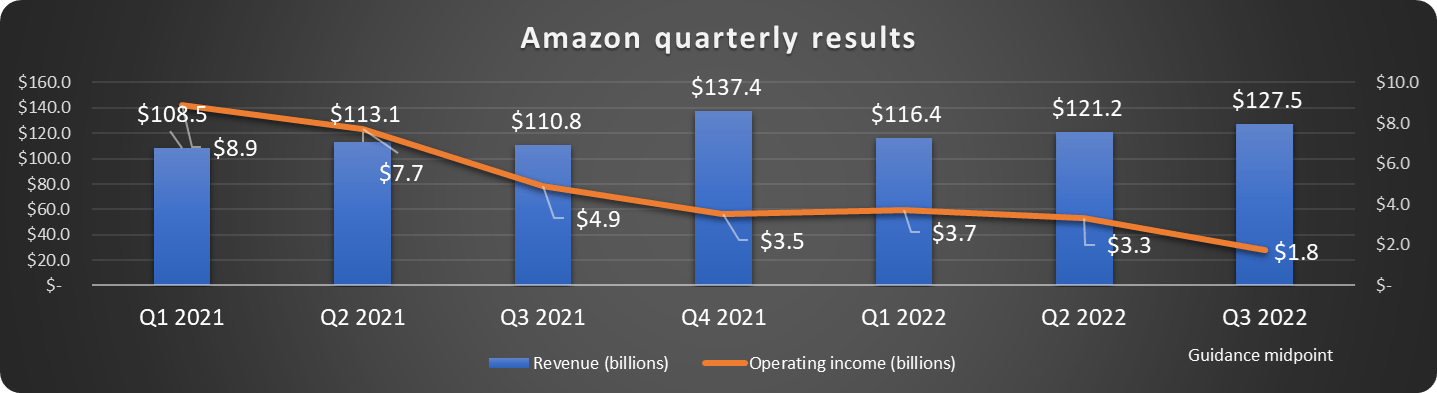

The company has forecast a 13-17% increase in revenue to $125-130 billion and operating income of $0-$3.5 billion. Revenue growth has not been an issue lately as shown below, but operating profit has been hard to come by.

Data source: Amazon and Seeking Alpha. Chart by Author.

Why is the operating result down?

Operating profit has taken a significant slump since the pandemic’s heyday. The initial surge in pandemic spending, economic stimulus and increased online shopping have given way to uncomfortable aftershocks.

First, while the company initially benefited from the stimulus that boosted the economy, rising wages and the tight labor market added billions of dollars in net costs. This was widespread in mid to late 2021 and is continuing.

Next, logistical issues plagued the supply chain for much of 2021, and challenges remain. This adds cost to already tight retail margins. This also contributes to inflation worldwide and in the US. We all know that inflation increases the cost of fuel and, well, just about everything else.

The strong US dollar had a massive impact on international results. Revenue in this segment declined 12% year-on-year (YOY) in the second quarter, but was down only 1% in constant currency. Operating income fell from a profit of $362 to a loss of $1.8 billion in the most recent quarter.

One more thing?

Management has done an admirable job in this challenging environment. Through the first half of 2022, gross margin is down just over 1%. In fact, the most significant cost increase is not compliance, as we might expect. Technology and content spending grew the most in the first half of 2022.

This is excellent news. Investments in technology and content, which include research for new products and servers, equipment, and other expenses for AWS and other companies, will drive future revenue and profits. Through the second quarter, Amazon spent $33 billion in this space, up 25% from the first half of 2021.

Check in to AWS

Amazon Web Services (AWS), the world’s largest provider of cloud services, is Amazon’s cash cow and has been its only consistent profit center of late. The segment had revenue of $19.7 billion and operating income of $5.7 billion for the most recent quarter. Amazon reported a run rate (annualized revenue) of $79 billion for AWS last quarter, and total revenue is likely to top $80 billion this year, with room to spare. Amazon’s cloud business consistently has operating margins close to 30%.

This segment has been so successful that it supports nearly all of Amazon’s $1.17 trillion market cap alone. The segment is up 35% so far in 2022 and, barring more drastic growth, will easily eclipse $100 billion in revenue in 2023 when there’s plenty of runway left.

AWS has a stranglehold on the cloud infrastructure market at over 33%, leading Microsoft (MSFT) Azure and Surpasses Alphabets (WELL)(Google) unprofitable Google Cloud.

Data source: Amazon. Chart and author’s estimates.

Microsoft is a profitable and growing software-as-a-service (SaaS) company that’s valued at about nine times its revenue. It’s more diverse and established than AWS, but not growing as fast.

I believe AWS could achieve a valuation of 9 to 10 times next year’s revenue, or $900 to $1 trillion, as an independent company in the open market. That means the rest of the company is relatively cheap right now.

Other quick hits

Expect AWS revenue to hit $21.4 billion if the company maintains second-quarter growth of 33%. Anything else would be a bit disappointing.

Ad growth has slowed somewhat, but was still resilient at 18% in the second quarter to reach $8.8 billion. Amazon has generated $34 billion in digital advertising revenue over the past 12 months, which is impressive considering where this revenue stream began. Revenues in this segment have been so insignificant that the company didn’t even report them separately until recently.

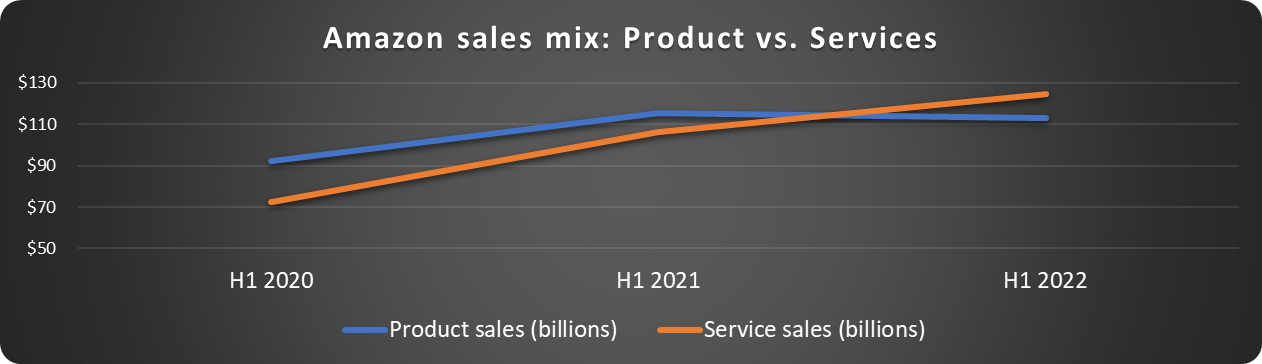

In 2022, total revenue from services surpassed product sales for the first time, as shown below.

Data source: Amazon. Chart by Author.

Why is that important? Service sales are higher margin and recurring, like AWS and memberships. This is fantastic news for shareholders. Hopefully this trend will continue and the gap will widen. A more services-centric Amazon will be more profitable, produce better cash flows, and make more money for shareholders.

Is Amazon stock a buy?

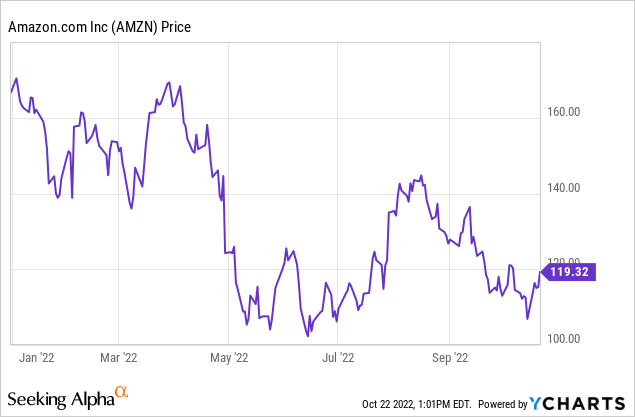

Amazon stock is down 30% year-to-date but has staged an 11% comeback from its recent low on Oct. 14, as shown below.

Ahead of the recent rally, I expected a strong positive reaction to earnings. There was just too much negativity priced in. Now we will see if the short-term rally has any legs.

Judging by the tone of the guidance for the most recent quarter, I wouldn’t be surprised if operating income came in on the low end of estimates. The massive success of AWS has increased infrastructure spending, which will increase depreciation costs and weigh on operating income. Because of this, the market might react negatively before digesting the details of the earnings report.

While the short-term move is always up for grabs, Amazon is still a solid long-term buy at these prices in my opinion. The rating is too convincing. The company continues to evolve into a services-based business that will grow margins and cash flow, and once the retail headwinds ease, the bottom line should rise massively and the stock price is likely to follow.